Titanium is the metal you reach for when you need strength like steel, weight closer to aluminum, and the ability to shrug off heat and saltwater. It forms a thin, tough oxide skin that protects it from corrosion, so it doesn’t rust in seawater or react badly with many fuels and chemicals. It also keeps its strength at temperatures where aluminum would soften, and it resists fatigue and crack growth after millions of load cycles. That unusual mix—light, strong, heat-tolerant, and corrosion-resistant—is why it’s critical in aerospace, defense, and now a lot of emerging tech. As these end markets scale, titanium’s strategic importance and pricing power rises. Meanwhile, its geopolitically exposed supply amplifies moats for the best-positioned players.

In this report, we highlight the top titanium stocks to watch, grouped by their position in the value chain.

We can start by splitting “titanium” into two very different worlds. Most of the planet’s titanium feedstock becomes titanium dioxide pigment—the ultra-white stuff in paints, plastics, paper, and sunscreen. That market lives on construction and consumer goods cycles.

This report instead focuses on the titanium metal chain—sponge, melt, forgings, fasteners, and qualified components—that feeds aerospace, defense, and high-spec industrial uses.

What drives demand for titanium metal?

- Aerospace is the primary demand driver. In airplanes and rockets, every kilogram matters. Using titanium in structures, landing gear, engine compressor parts, and critical fasteners trims weight without giving up safety margins. It’s also a good neighbor to carbon-fiber composites: aluminum can corrode when it touches carbon fiber, but titanium holds up much better. When you hear about Airbus or Boeing raising monthly build rates, that’s the sound of the titanium value chain spooling up.

- Defense adds a sticky, sometimes counter-cyclical layer. Defense leans on titanium for the same reasons as aerospace, plus a few more. Titanium delivers serious protection for its weight, so it shows up in armor and hardened structures. It’s non-magnetic and highly resistant to seawater, which makes it valuable for naval hardware and submarines that can’t afford corrosion. Its high fatigue strength is also a big deal for aircraft that pull heavy G-loads and for missiles and drones that see sharp maneuvers.

- The sleeper driver is inventory behavior. If buyers fear disruption, they restock and double-order beyond end-use needs. This is the classic “bullwhip” effect, where small changes at the consumer create big swings upstream.

Many frontier technologies are quietly built on titanium, too.

- eVTOLs and long-range drones use it to keep airframes light and durable.

- Reusable rockets, hypersonic vehicles, and space hardware need materials that survive heat and vibration without adding mass—again, a titanium sweet spot.

- Offshore wind, geothermal, and next-gen nuclear systems use titanium where salt, heat, or aggressive fluids would chew up other metals.

- In medical tech, its biocompatibility makes it the go-to for implants.

- In batteries and energy storage, certain titanium compounds enable long-life electrodes.

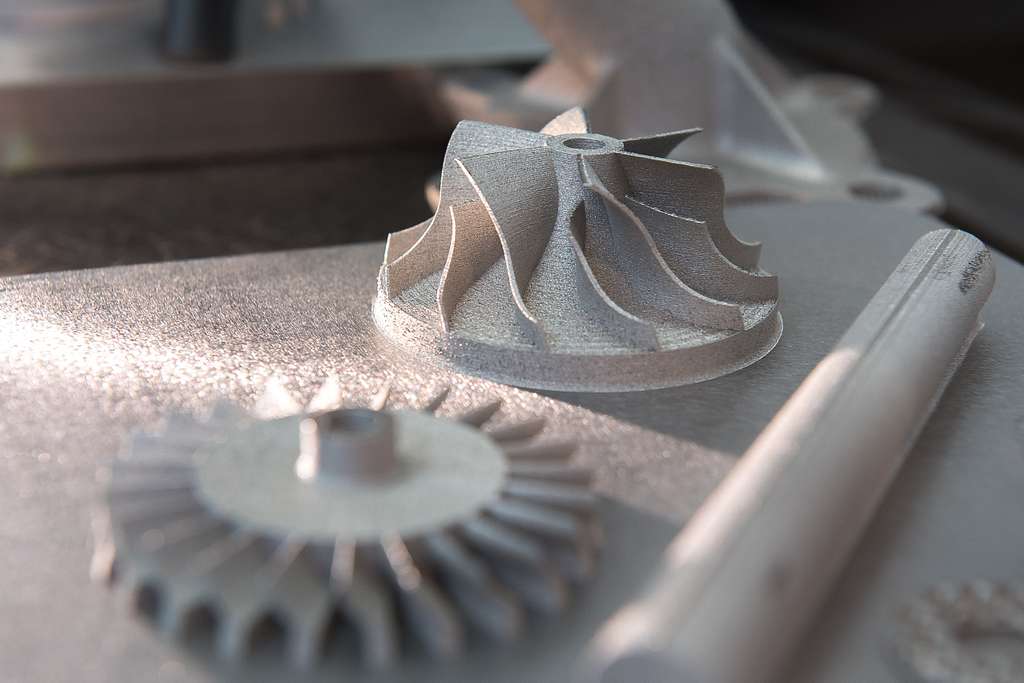

- Additive manufacturing is a fast-growing niche: powdered Ti-6Al-4V parts let designers create intricate, hollow, or lattice parts while cutting weight and consolidating assemblies. Some of these designs were almost impossible to make before 3D metal printing.

Net-net: watch aircraft build rates, engine deliveries, defense awards, and restocking behavior—when several flash green together, titanium demand can outrun forecasts fast. Frontier markets won’t drive tonnage near term, but they punch above their weight in mix, pricing power, and long-term optionality.

How do supply chain chokepoints and geopolitics come into play?

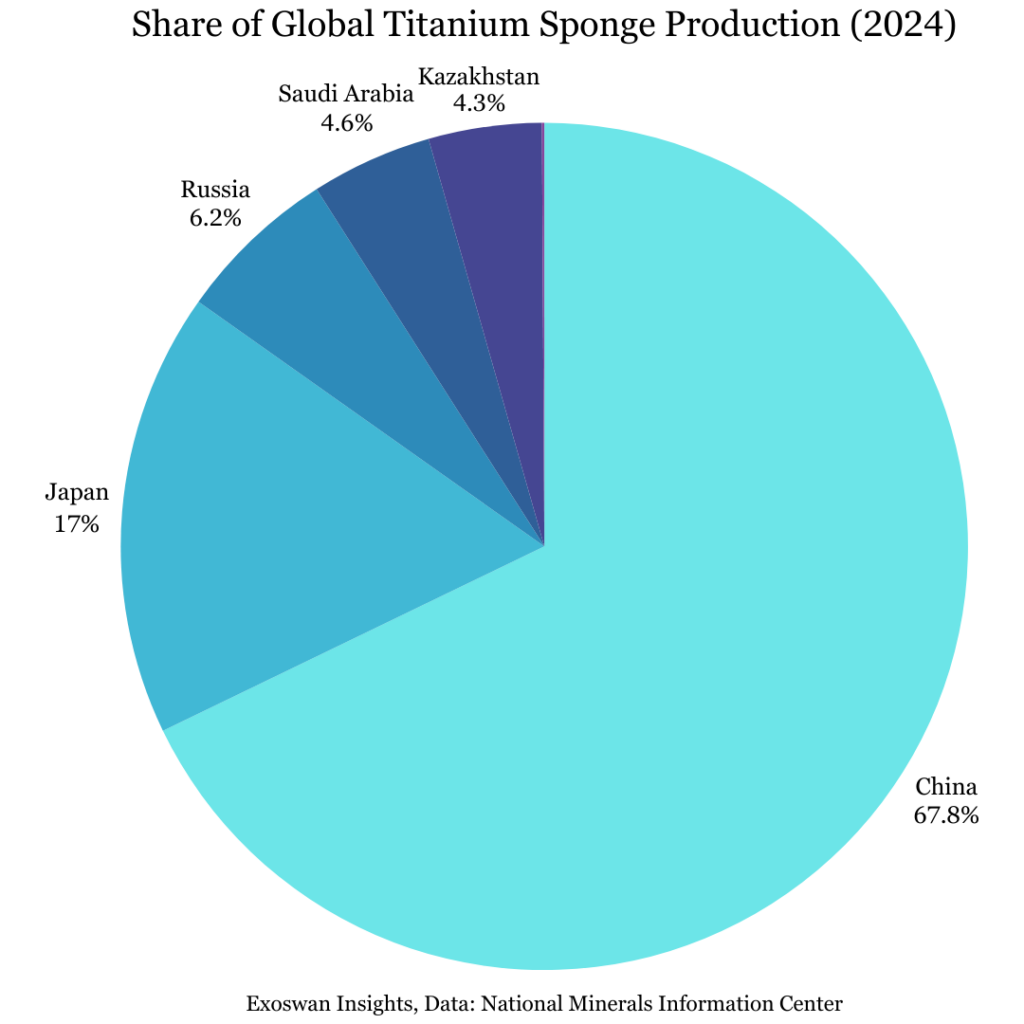

Titanium’s supply chain is narrow and picky, and that’s what turns it into a geopolitical pressure point. Making flight-worthy titanium isn’t just “dig ore, make metal.” It runs through a small set of steps: mineral sands → chlorination → sponge (via the Kroll process) → melted ingot → forged/machined parts. At several of those steps, there are only a handful of qualified players. The U.S., for example, shut its last sponge plant in 2020 and has relied on imports ever since, especially from Japan.

For two decades the biggest single chokepoint was Russia’s VSMPO-AVISMA. Before the war in Ukraine, it supplied a large slice of the world’s aerospace titanium and was deeply embedded with both Boeing and Airbus. Boeing stopped buying Russian titanium in early March 2022; Europe moved more cautiously because Airbus still depended on it. The result is a supply chain that’s still digesting a major reroute.

“Why not just buy from China?” is the obvious question. China now produces a lot of sponge, but aerospace is about proven pedigree: materials and mills must be qualified, sometimes part-by-part, which takes years. Chinese sponge still isn’t broadly accepted for critical aerospace uses, and new supplier approvals can run 1–3 years for structural grades and 5+ years for engine-rotation (“prime/rotating-quality”) routes. That lag, not raw tonnage, is the bottleneck.

Basically, the upstream picture looks like this:

- Russia remains a technically capable, heavily integrated supplier whose metal is entangled with sanctions politics. Western buyers have tried to decouple, but you can’t shortcut qualification.

- Japan is the quiet cornerstone. Toho Titanium and Osaka Titanium keep the U.S. and Europe supplied with high-spec sponge and mill products. Saudi output via a Toho joint venture has been ramping, adding some resilience.

- Kazakhstan’s UKTMP remains one of a very small number of producers qualified across aerospace chains, useful but finite.

- China is huge in volume but, for now, only partly accepted in Western aerospace. Policy shifts or new certifications there could reshape the map quickly.

What’s being done? Planemakers are dual-sourcing parts and moving more work to non-Russian suppliers. Governments are also trying to rebuild domestic capacity and recycling: the U.S. DoD funded projects to stand up a domestic mine-to-metal chain. And in Europe, policymakers are pushing “circular” titanium, which involves recovering and upgrading machining scrap to trim reliance on primary sponge. None of these are overnight fixes, but they chip away at the chokepoints.

All this results in a supply chain that’s slow and costly to reroute. The following titanium stocks are positioned at different steps of this chain, poised to benefit from “friend-shoring” tailwinds and stringent qualification moats.

Titanium Sponge Producers

Sponge producers sit at the start of the titanium supply chain for aerospace and defense. These companies produce the raw, high-purity titanium sponge that everyone else depends on. These titanium stocks are a pure-play bet on the foundational raw material and its strategic importance. Control over this production bottleneck provides significant geopolitical leverage.

Toho Titanium (TSE: 5727)

HQ: Japan; Cornerstone supplier of flight-qualified titanium sponge.

Toho Titanium is the quiet cornerstone of the Western titanium metal chain. It’s one of the best-known sources of flight-qualified sponge and high-purity titanium, the raw starting point for the ingots, forgings, and fasteners that go into airframes and engines. That matters more than ever as Airbus, Boeing, and their suppliers work to diversify away from Russian material; every extra qualified tonne reduces a bottleneck that’s been slowing the system.

What really differentiates Toho is its global footprint and product breadth. At home in Japan it’s a long-standing supplier into aerospace, but its Saudi joint venture in Yanbu adds a sizable, “friend-shored” sponge source—about 15.6 kt per year, roughly 10% of global output—plugged straight into Red Sea export lanes. That extra node gives the industry redundancy without compromising on pedigree. Toho also straddles adjacent high-spec niches (like semiconductor-grade, high-purity titanium), which tend to support margins and keep the company close to frontier-tech customers. Net-net, Toho is positioned as a scarce, qualified supplier with growing, geographically diverse capacity.

Osaka Titanium (TSE: 5725)

HQ: Japan; Sponge plus ultra-pure titanium for semiconductors and aerospace.

Osaka Titanium is a pure-play on the metal itself: a focused sponge maker with a reputation for stable, high-quality supply into aerospace, plus a distinctive second engine in ultra-high-purity titanium for electronics. That combo—flight-grade sponge and 4N–5N purity titanium used to make sputtering targets—gives Osaka leverage to two powerful demand lanes at once: the ongoing aerospace upcycle and structurally rising semiconductor content.

Its other edge is form factor know-how. Osaka has been producing low-oxygen, gas-atomized titanium powders for decades, supplying exacting uses in displays and metal injection molding and increasingly feeding additive manufacturing. As 3D-printed Ti-6Al-4V parts move from prototypes to production in aerospace, medical, and energy, customers tend to favor veteran powder suppliers with tight oxygen control and consistent flow. That positions Osaka as a natural beneficiary of the metal-printing shift, on top of the conventional melt-route business. Osaka’s focused portfolio is a clean way to own the titanium metal theme with meaningful exposure to next-gen manufacturing.

Integrated Titanium Processors

This category of titanium stocks contains the industrial giants of the industry. They take raw sponge and melt, forge, and mill it into usable industrial forms. These firms form the backbone of the Western supply chain, protected by immense capital requirements and decades-long aerospace qualifications, making them core holdings for exposure to the entire value chain.

ATI Inc. (NYSE: ATI)

HQ: USA; Aerospace-focused titanium and specialty alloys powerhouse.

ATI Inc. is a pure play on the “friend-shored” titanium and high-temperature alloy chain that feeds jets, engines, and defense. Since acquiring RTI, ATI has the melt capacity, mill products, and closed-loop scrap ecosystem to turn titanium into qualified billet, plate, and near-net shapes that slot straight into airframes and engine-adjacent hardware. The company’s center of gravity sits right where demand is compounding: rising Airbus/Boeing build rates, more engines shipping, and defense programs that prize fatigue strength and corrosion resistance.

ATI’s long tenure with primes and tier-ones means deep approvals and sticky positions—exactly what matters when the world is diversifying away from Russian supply and buyers want Western, proven pedigree. Mix matters here: titanium for structures and fasteners rides the aircraft ramp, while ATI’s broader high-temp alloys keep it tied to engine spares and upgrades, smoothing cycles. Add in the quiet tailwinds—inventory restocking, additive manufacturing, and frontier tech—and ATI looks leveraged to both volume and value. It’s an advantaged node in a narrow supply chain, with operational know-how that’s hard to copy and customer switching costs that rise with every additional approval.

TIMET (via Berkshire Hathaway, NYSE: BRK.A)

HQ: USA; Vertically integrated aerospace-grade titanium producer.

TIMET is the titanium backbone tucked inside Berkshire’s Precision Castparts ecosystem. Its sponge-to-melt-to-mill integration feeds one of the world’s most entrenched aerospace and defense supply chains. That vertical setup is strategic: it gives airframe and engine customers assurance on quality, pedigree, and delivery, and it lets TIMET point scarce capacity at the highest-value orders as build rates climb. Decades of qualifications across structural and fastener routes make TIMET a default choice when programs dual-source away from Russia and want a Western supplier with deep process control.

The Berkshire umbrella adds balance-sheet strength and a captive downstream customer in forgings and complex components, tightening the loop between titanium chemistry, microstructure, and finished part performance. As commercial fleets grow and defense platforms stay funded, TIMET benefits from both tonnage and mix—more titanium per aircraft as composites expand, and more recurring demand from engines, missiles, submarines, and long-life naval hardware. Restocking behavior can add upside: when buyers worry about disruption, they pull forward titanium, and TIMET’s approvals mean those purchase orders land close to home. It’s a classic “local monopoly” dynamic in high-spec materials—sticky positions, long programs, and a moat built on metallurgy, not marketing.

Kobe Steel, Ltd. (TSE: 5406)

HQ: Japan; Qualified titanium mill products for aerospace and industry.

Kobe Steel is Japan’s titanium workhorse, turning qualified feedstock into premium sheet, plate, and forged products that live where seawater, heat, and fatigue would punish lesser metals. The company sits at the crossroads of two durable growth engines. First is aerospace: as Airbus and Boeing raise rates, titanium rides along in landing gear, structures, and critical fasteners—especially where it pairs cleanly with carbon-fiber composites. Second is high-spec industrial: desalination, plate heat exchangers, offshore wind, geothermal, and advanced chemical plants all lean on titanium’s corrosion resistance for life-cycle economics.

Kobe’s edge is process: tight control from melting through rolling and finishing, long-standing certifications, and close engineering ties with Japanese sponge producers and global primes. That translates into reliable quality and predictable lead times—gold in a supply chain that’s still rerouting away from Russia and remains selective about Chinese pedigree for flight-critical parts. Add emerging niches—additive Ti-6Al-4V components, eVTOLs, reusable space hardware—and Kobe’s portfolio tilts toward higher-margin, higher-spec applications over commodity volumes. With entrenched relationships in Asia, Europe, and the U.S., Kobe is positioned as a dependable, scale Japanese node in a friend-shoring world where trust and qualification are the real currency.

Value-Added Components & Alloys

This group of titanium stocks represents the final, highest-margin step in the titanium metal supply chain. These companies don’t make the metal itself; they use deep engineering expertise to turn it into finished, flight-critical components and specialized alloys. These companies derive their moat from intellectual property, manufacturing prowess, and sticky certifications.

Howmet Aerospace (NYSE: HWM)

HQ: USA; Flight-critical titanium fasteners, castings, and rings specialist.

Howmet sits at the “last mile,” where titanium turns into irreplaceable hardware. Its franchise is flight-critical fasteners, structural castings, and seamless rings that are designed into the airframe and engine from day one. That design-in status matters: once a fastener system or near-net titanium component is qualified on a jet, it tends to stay there for decades and across derivative models. Howmet’s edge is the combination of materials know-how (titanium behavior in hot, corrosive, and cyclic environments), proprietary manufacturing routes, and the paperwork moat of aerospace qualifications.

As Airbus and Boeing lift build rates and engine makers push hotter, lighter architectures, Howmet captures more “content per shipset” in titanium bolts, collars, lugs, and structural forms that marry well with carbon-fiber airframes. It also benefits from friend-shoring as primes diversify away from historically concentrated suppliers—Howmet is often the Western “safe pair of hands” for titanium parts that can’t fail. Add in aftermarket pull-through (fasteners and replacement hardware wear out and get refreshed on heavy checks) and exposure to newer platforms like eVTOLs and long-range drones, and you get a business that compounds with every incremental airplane and every new lightweight design choice.

Carpenter Technology (NYSE: CRS)

HQ: USA; Premium titanium and specialty alloys melt-process leader.

Carpenter is the metallurgical engine behind premium titanium and specialty alloys. Where Howmet shines in finished parts, Carpenter differentiates at the melt: vacuum systems, tight chemistries, and quality routes (VIM/VAR/PVAR) that produce aerospace-grade titanium and adjacent superalloys, including rotating-quality material for engines and high-integrity bar, billet, and powder for additive manufacturing. That capability is scarce and slow to replicate because the “product” isn’t just metal—it’s proven pedigrees, heats, and traceability that pass the most demanding certifications in aerospace, defense, medical, and energy.

As aircraft and missiles chase weight savings and fatigue life, Carpenter wins on custom chemistries and consistent microstructures that downstream forgers and machine shops trust. The company benefits directly from rising narrowbody build rates, but also from mix: newer platforms and 3D-printed Ti-6Al-4V components pull higher-value inputs. Carpenter’s role as a U.S. supplier with deep qualification libraries makes it a natural partner for supply-chain re-shoring and dual-sourcing. In short, it’s the materials science partner that feeds the rest of the titanium chain.

TriMas (NASDAQ: TRS)

HQ: USA; High-mix titanium aerospace fasteners for assembly speed.

TriMas is rooted in the titanium theme through TriMas Aerospace—the specialist for high-mix, engineered fasteners and small titanium parts that make final assembly go faster and safer. Its differentiation is speed and specificity: proprietary blind bolts, rivets, collars, and precision hardware tuned for composite-rich structures where titanium beats aluminum on galvanic corrosion and strength-to-weight. These are the “last-inch” components: low dollar each, but mission-critical and heavily qualified, with designs embedded in work instructions at OEMs and Tier-1s. That creates sticky positions across legacy fleets and new programs alike, plus steady aftermarket cadence as fleets cycle through maintenance checks.

TriMas leans into short lead times, automation, and cell-based manufacturing to service hundreds of SKUs reliably—a valuable niche when the broader supply chain is tight. As Airbus and Boeing step up monthly rates, as defense airframes and UAVs proliferate, and as eVTOL makers standardize on lightweight, corrosion-proof fastening systems, TriMas’ titanium content scales with every additional hole drilled in a wing, fuselage, pylon, or nacelle. Compared with alloy makers and large casting houses, TriMas wins by being the nimble problem-solver at the line—owning thousands of tiny, qualified decisions that keep build tempo high.

Titanium Tech & Additive Manufacturing

This segment is focused on the future. These companies are not part of the traditional supply chain; they are trying to disrupt it with new technologies. From novel methods for making cheaper powder to 3D printing complex parts, these titanium stocks represent a higher-risk, higher-growth bet on a more efficient and sustainable manufacturing paradigm.

IperionX (NASDAQ: IPX)

HQ: USA; Vertically integrated titanium powders and additive parts.

IperionX is building the U.S. titanium comeback story, aimed squarely at the chokepoints that hold back aerospace, defense, and advanced manufacturing. The company’s Virginia Titanium Manufacturing Campus is designed to take scrap titanium and U.S. mineral feedstock and turn it into low-carbon powders and near-net-shape parts using HAMR—a de-oxygenation route that targets lower cost and energy versus legacy methods. With the HAMR furnace commissioned and the broader campus equipment online, the site is positioned as a domestic source for powders and components. That matters because the Pentagon is explicitly funding a home-grown titanium chain: IperionX secured a DoD award of up to $47.1M to accelerate capacity in Virginia.

Demand signals are also real on the commercial side. Ford selected IperionX to supply additively manufactured titanium components for future performance vehicles—an early proof point that recycled, lower-carbon titanium can win its way into high-spec programs beyond aerospace. If the next cycle is about resilient supply, then a domestic, circular titanium platform with powder metallurgy at its core is well placed. IperionX’s thesis is simple: de-risk the titanium bottleneck for U.S. industry, monetize powders and qualified parts into sticky defense and mobility programs, and let build-rate growth and friend-shoring do the compounding.

Titomic Ltd. (ASX: TTT)

HQ: Australia; Cold spray titanium for large structures and rapid repair.

Titomic is the pure-play on cold-spray metal AM scaling up for aerospace, defense, and harsh-environment industries. Its Titomic Kinetic Fusion™ (TKF) process accelerates metal powders to supersonic speeds and bonds them without melting—enabling fast deposition, low heat input, and very large structures or repairs that are hard to do with laser or wire processes. Over the past year, Titomic helped co-develop the first SAE aerospace standard for cold-spray AM (AMS 7057), a key trust-building step that shortens qualification cycles and moves cold spray from “promising” to “specified.” At the same time, the company planted its flag in the U.S., opening a 59,000-sq-ft facility in Huntsville, Alabama—right inside America’s defense-aerospace neighborhood.

Titomic is also stitching together the go-to-market fabric: teaming with REPKON USA on defense applications and collaborating with Metal Powder Works for powder supply and process breadth. The thesis here is that as fleets age, shipyards expand, and missiles/space hardware ramp, cold-spray AM becomes a strategic tool for rapid production, coatings, and sustainment—especially for titanium where heat and oxidation complicate conventional routes. With a standard in place and U.S. manufacturing onshore, Titomic can convert pilot wins into recurring production and repair programs.

AML3D (ASX: AL3)

HQ: Australia; Wire-arc 3D printing for large certified parts in defense and utilities.

AML3D is commercializing large-format wire-arc additive manufacturing (WAAM) through its ARCEMY® systems, and it’s finding product-market fit in the U.S. Navy. The company has sold and commissioned multiple ARCEMY units into the submarine and surface-ship supply chain via BlueForge Alliance and key suppliers like Laser Welding Solutions, turning WAAM into a practical path for certified, heavy-section parts and rapid replacements. A marquee proof point: AML3D’s largest custom ARCEMY system went online at Austal USA’s Additive Manufacturing Center of Excellence, supporting efforts to embed AM deeper into naval sustainment and new-build workflows.

Recent orders and collaborations (from portable ARCEMY systems to Navy LOIs) underline growing demand for on-site or near-site metal AM that can cut lead times from months to days. The aim here is to be in the right lane of re-industrialization: shipyards, submarine programs, and prime contractors need qualified, big-build metal AM that’s simpler to run, material-efficient, and deployable at the point of need. AML3D’s WAAM platform—focused on certified feedstocks, parameter control, and production-grade cells—gives it leverage as defense sustainment scales and as utilities, energy, and heavy industry catch on to the same uptime economics.