Nuclear power supplies nearly 20% of America's electricity. Yet it's been the sleeping giant of the clean energy revolution, hobbled by a 40-year stagnation in fleet growth. The reason: gigawatt-scale plants became synonymous with decade-long delays and budget overruns. Today, that calculus is being rewritten by Small Modular Reactors (SMRs). This new class of reactor is poised to unlock nuclear power just as a dual crisis—soaring power demand from AI and global energy insecurity—forces a worldwide reappraisal of energy strategy.

This report highlights the top small modular reactor stocks to watch: factory-built nuclear to solve the AI power crunch & provide Western energy sovereignty.

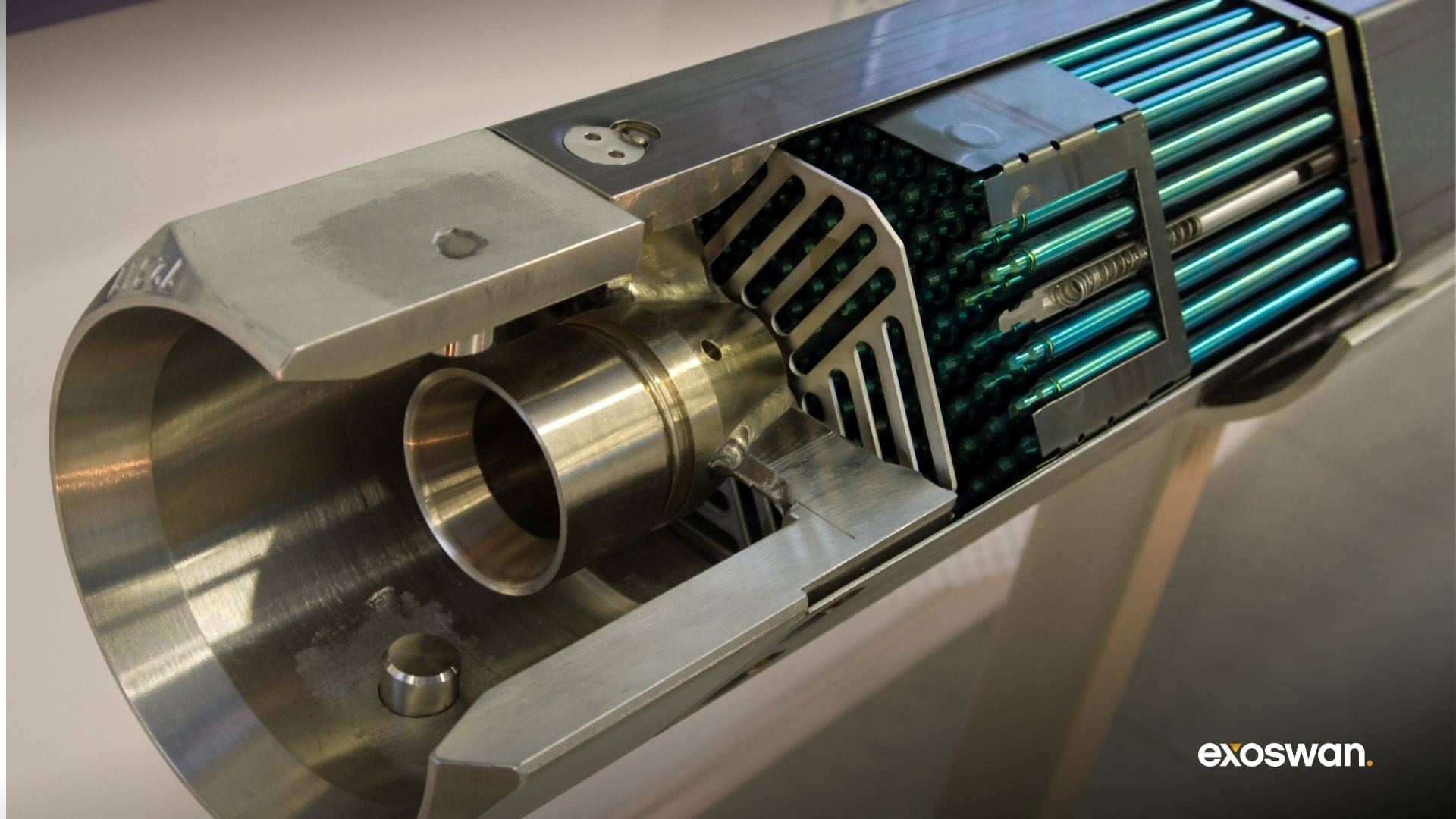

What's so special about small modular reactors?

A traditional nuclear plant was like building a custom cathedral—each one unique, time-consuming, and prone to massive cost overruns. SMRs, by contrast, are built like cars on an assembly line. This factory-first approach unlocks a learning curve, making the 10th and 100th units progressively cheaper and faster to build than the first.

Because they're much smaller than traditional nuclear reactors, they can also be installed in previously inaccessible places. Think: tech campuses, industrial sites, or even strategic military bases. This far expands their addressable market over legacy nuclear. Since they're modular, they can be scaled for each deployment without requiring bespoke engineering.

Finally, SMRs benefit from “walk-away safe” designs that rely on simple physics—like gravity and natural water circulation—for cooling, eliminating complex safety pumps. This combination of inherent safety, size, and manufacturing predictability have made SMRs a rising star of next-gen nuclear technologies.

Why SMRs, Why Now?

First, the world faces an acute power deficit, driven by the explosive growth of AI data centers. The International Energy Agency projects data center energy consumption to more than double to about 945 terawatt‑hours by 2030. Wind and solar are cheap but intermittent; batteries can stretch them only so far. Grid operators and big tech thus are looking for clean baseload power to keep AI clusters humming 24/7. SMRs slot neatly into that gap: compact enough to sit beside a tech campus, yet steady enough to guarantee five‑nines reliability without carbon emissions or local air pollution.

Policy and geopolitics supply the second big push. Analysts now frame SMRs as a way to “neutralize Russia’s influence” on Europe via gas. Washington has moved just as aggressively: the U.S. Department of Energy’s Advanced Reactor Demonstration Program is pouring hundreds of millions into first‑of‑a‑kind SMR projects. The U.S. and U.K. also recently signed a landmark Technology Prosperity Deal to streamline regulation and accelerate joint development of advanced nuclear technologies, explicitly to secure Western energy supply chains.

In essence, small modular reactors promise nuclear’s reliability, at a fraction of the price and complexity—all while solidifying energy sovereignty. Let's look at the companies best positioned to ride these tailwinds.

Pure-Play SMR Developers

These companies are the vanguard of the nuclear renaissance, dedicated exclusively to developing and commercializing specific SMR designs. Pure-play small modular reactor stocks offer the most direct exposure to the technology’s potential but also carry the highest risk. Many are pre- or early- revenue, navigating regulatory and first-of-a-kind engineering hurdles where not all will survive.

Currently, there’s one publicly traded pure-play (NuScale), alongside several key private players that serve as bellwethers for the sector.

NuScale Power (NYSE: SMR)

HQ: USA; First-mover with the earliest NRC-certified SMR design.

NuScale Power, the first company with a U.S. Nuclear Regulatory Commission (NRC) certified design, has a critical first-mover advantage. Its VOYGR power plant is a pressurized light-water reactor (LWR) based on decades of proven technology. Each power module is a self-contained unit generating 77 MWe, allowing for scalable plants up to a 924 MWe (12-module) facility. This modularity offers utilities flexibility to replace retired coal plants. The design’s core innovation is its passive safety system, which uses natural convection to cool the reactor indefinitely without operator action, external power, or additional water—a feature instrumental in its regulatory approval.

NuScale is converting its regulatory lead into commercial momentum. In a landmark announcement in September 2025, the company revealed a partnership with ENTRA1 Energy and the Tennessee Valley Authority (TVA) for a massive 6-gigawatt SMR deployment program. This follows established projects like RoPower in Romania, supported by international financing. Positioned as the most mature SMR technology, NuScale represents the bridge between the legacy nuclear industry and the new paradigm of factory-built, scalable power, making it a go-to partner for risk-averse utilities.

TerraPower (Private)

HQ: USA; Advanced reactor with integrated storage for flexible grid power.

Founded by Bill Gates, TerraPower is developing one of the most technologically ambitious and closely watched advanced reactors. Its flagship Natrium reactor is a 345 MWe sodium-cooled fast reactor, a Generation IV design that operates at higher temperatures and lower pressures for enhanced efficiency and safety. Its standout feature is an integrated molten salt thermal energy storage system, allowing the plant to flex its output to 500 MWe for over five hours. This capability lets the Natrium reactor act as a "nuclear battery," dispatching firm power to balance intermittent renewables, making it highly attractive for modern grids.

TerraPower's strategy centers on its Natrium Reactor Demonstration Project in Kemmerer, Wyoming, the site of a retiring coal plant. After breaking ground in 2024, the company is on an aggressive construction timeline, with the NRC's final safety evaluation expected by mid-2026. Backed by a recent $650 million funding round and strategic partnerships with data center operator Sabey and engineering firm KBR, TerraPower is building a repeatable deployment model. The company's influential founder, innovative storage technology, and progress on its first build position it as a leader in advanced nuclear energy.

X-energy (Private)

HQ: USA; High-temperature gas reactor for valuable industrial heat applications.

X-energy is a front-runner in developing high-temperature gas-cooled reactors (HTGRs), a technology prized for its versatility and inherent safety. Its Xe-100 reactor is an 80 MWe unit, scalable to a four-pack 320 MWe plant. The reactor uses helium to reach temperatures over 750 °C, making it ideal for both electricity generation and high-temperature steam for industrial applications like hydrogen production. Its safety case is anchored by proprietary TRISO-X fuel, a robust particle fuel that is physically incapable of melting down.

X-energy has secured both commercial and government backing. A landmark Joint Development Agreement with Centrica, announced in September 2025, aims to deploy up to 12 Xe-100 reactors in the United Kingdom. In the U.S., it is partnered with Dow Inc. for a demonstration project at a Gulf Coast chemical facility. The company has also forged an alliance with Amazon, Korea Hydro & Nuclear Power, and Doosan Enerbility to explore powering AI infrastructure. With its versatile industrial applications, meltdown-proof fuel, and strong international partnerships, X-energy takes aim at the resilient market for industrial heat and power.

Nuclear Microreactors

A subset of SMRs, microreactors target a distinct market for compact power sources, typically under 50 MWe. This segment focuses on niche applications like remote industry, military bases, and dedicated data centers, promising a faster, factory-driven path to deployment. Prospects for these specialized small modular reactor stocks depend on whether this novel technology can unlock a market large enough to justify its development costs.

Oklo Inc. (NYSE: OKLO)

HQ: USA; Microreactor with a power-as-a-service model for AI.

Oklo is at the forefront of the microreactor segment, targeting the market for compact, reliable power. Its Aurora powerhouse is a liquid metal-cooled fast reactor designed to run for over a decade without refueling. Initially a 1.5 MWe unit, Oklo recently announced an upsized 75 MWe design to meet surging demand from AI data centers. Aurora's key attributes are its simplicity, autonomous operation, and a "power-as-a-service" model where Oklo owns and operates the reactors, selling electricity under long-term contracts. This removes the high upfront capital cost for clients, making nuclear power accessible to new industrial and commercial users.

After an initial regulatory setback, Oklo is poised for a major comeback, planning to submit a combined license application to the NRC in late 2025. The company has secured powerful allies, including a "master power agreement" to supply up to 12 GW of power to data center giant Switch and a contract with the U.S. Air Force for a microreactor at Eielson Air Force Base. Oklo offers an asset-light model and direct exposure to AI power demand.

NANO Nuclear Energy (NASDAQ: NNE)

HQ: USA; Mobile microreactors targeting secure defense and government contracts.

NANO Nuclear Energy develops portable and versatile microreactors for remote and defense applications. The company recently streamlined its strategy, selling its "ODIN" design to focus on its gas-cooled microreactor portfolio. Its flagship project is the "KRONOS" mobile microreactor, a high-temperature gas-cooled reactor designed for rapid transport and deployment. This focus on mobility and resilience makes it a strong candidate for powering remote communities, mining operations, and military bases, providing energy security in contested environments.

NANO is actively engaging with regulators and has entered the pre-application process with the U.S. NRC. The company has cultivated deep ties within the national security apparatus, securing a Cooperative Research and Development Agreement (CRADA) for a project at Joint Base Anacostia-Bolling. A recent $105 million fundraising round in June 2025 provides the capital to advance its engineering and licensing. By targeting the unique energy needs of the Department of Defense, NANO is carving out a defensible niche in the microreactor market.

Last Energy (Private)

HQ: USA; Fully managed, factory-built microreactors for industrial customers.

Last Energy is built on a radical premise: to make nuclear simple and scalable through mass manufacturing and a streamlined delivery model. The company's core innovation is not its reactor technology—a standard 20 MWe pressurized water reactor—but its end-to-end “power plant in a box” product. Last Energy delivers a fully assembled, factory-built microreactor power plant, handling everything from licensing to operations. The company's strategy is to bypass the lengthy U.S. NRC licensing process by focusing initially on European markets with more streamlined regulatory frameworks.

This international-first strategy is succeeding. Last Energy's most significant commercial breakthrough is its partnership with DP World, one of the world's largest port operators, to develop a microreactor plant at the London Gateway port in the U.K. This project provides a powerful reference case for powering critical infrastructure. The company has also signed agreements for potential projects in Poland and Romania. By prioritizing speed to market and a fully managed product, Last Energy is positioning itself as the most accessible on-ramp to nuclear energy for industrial customers.

SMR Critical Enablers

This segment represents the "picks and shovels" of the nuclear buildout, providing essential fuel, components, and services. These companies profit from the sector's overall growth regardless of which reactor designs ultimately win. For those seeking a de-risked approach, these enablers offer a broader bet on the success of small modular reactor stocks as a whole.

Centrus (NYSE: LEU)

HQ: USA; Sole Western HALEU producer, the critical advanced reactor fuel.

Centrus is arguably the single most critical enabler of the advanced nuclear industry in the West. It’s the only company outside of Russia licensed to produce High-Assay, Low-Enriched Uranium (HALEU), the fuel required by most next-generation reactor designs. This gives Centrus a near-monopolistic position at a strategic choke point in the nuclear fuel cycle. The geopolitical imperative to decouple from Russian fuel has transformed Centrus from a legacy enricher into a cornerstone of U.S. national and energy security. Its Piketon, Ohio, facility began HALEU production in 2023 and is ramping up output under contract with the U.S. Department of Energy.

Centrus has achieved key operational milestones, delivering 900 kg of HALEU to the DOE as of June 2025 and securing a contract extension through mid-2026. The company boasts a $3.6 billion order book for traditional enrichment services, providing a stable financial foundation. As advanced reactors move to deployment, demand for HALEU is set to ramp, and Centrus is the only licensed domestic supplier ready to meet it. This makes Centrus an essential toll collector for the advanced nuclear industry.

Lightbridge Corp (NASDAQ: LTBR)

HQ: USA; Advanced metallic fuel designed to uprate existing reactors.

Lightbridge is a nuclear fuel technology company developing a metallic fuel to improve the economics and safety of existing reactors and future SMRs. Its patented fuel is a helically twisted, metallic rod of a zirconium-uranium alloy. This design has better thermal conductivity than traditional ceramic fuels, allowing reactors to operate at lower temperatures and generate more power. The company projects its fuel can deliver a 17% power uprate and longer fuel cycles for existing reactors, generating substantial additional revenue for utilities. For new SMRs, the fuel's enhanced safety characteristics could streamline licensing and reduce capital costs.

Lightbridge's strategy is to be a pure-play intellectual property provider, licensing its fuel designs to major fabricators. The company is collaborating with U.S. national labs, including a long-term framework agreement with Idaho National Laboratory, for the rigorous testing needed for NRC certification. With a strong cash position of nearly $98 million as of mid-2025 and no debt, the company is well-capitalized to complete its multi-year development.

BWX Tech (NYSE: BWXT)

HQ: USA; Indispensable manufacturer for the entire nuclear supply chain.

BWX Technologies is a dominant force in the U.S. nuclear manufacturing supply chain. With a century-long history, it’s the sole manufacturer of naval nuclear reactors for the U.S. Navy's submarines and aircraft carriers, a role that has given it unparalleled expertise in precision manufacturing. This experience makes BWXT an indispensable partner for the SMR industry. It’s a leading manufacturer of the large, heavy components—like reactor pressure vessels—that form the heart of a nuclear plant. The company could thus become the premier "foundry for SMRs," leveraging its existing facilities to supply multiple developers.

BWXT's strategic importance was underscored by a $1.5 billion NNSA contract in mid-2025 to establish a domestic uranium enrichment capability for defense purposes, cementing its role in the national security supply chain. In the commercial space, it is a key partner to several reactor developers, including a collaboration with Kairos Power for commercial TRISO fuel manufacturing. BWXT represents a "picks and shovels" play on the entire nuclear sector, poised to benefit regardless of which specific reactor designs ultimately win the race.

Diversified Industrials with SMR Programs

These are established industrial titans that are developing SMRs as a strategic growth engine within a much larger business. An investment here is less a bet on a single technology and more on a diversified company's ability to execute. While their SMR programs offer upside, these aren't pure-play small modular reactor stocks; their nuclear ambition is diluted by legacy operations.

GE Vernova (NYSE: GEV)

HQ: USA; Bankable SMR from a global leader nearing deployment.

GE Vernova, in a joint venture with Hitachi, is leveraging its deep institutional knowledge to commercialize its BWRX-300 SMR. The 300 MWe reactor is a boiling water reactor, a design that builds directly on the lineage of GE's licensed, operating reactors. This evolutionary approach significantly de-risks the technology and regulatory pathway. The BWRX-300 design is radically simplified compared to its predecessors, reducing the volume of concrete and steel needed for a much smaller footprint. This focus on "Design-to-Cost" makes it one of the most economically competitive SMR designs on the market.

GE Vernova's strategy leverages its global footprint and existing utility relationships. The company achieved a critical milestone in North America: its partner, Ontario Power Generation, received a construction license from Canada's nuclear regulator in April 2025 for the first BWRX-300 at its Darlington site, with a 2029 target in-service date. The company is pursuing deployments globally, with agreements in Estonia and advanced discussions in Poland, the U.K., and the U.S., including a potential TVA build at Clinch River. With a licensed, cost-competitive design and a clear path to first power before 2030, GE Vernova is the incumbent leader bringing a pragmatic, bankable SMR to the global market.

Rolls-Royce Holdings (LSE: RR)

HQ: UK; National champion with government backing and a factory-first model.

Rolls-Royce, with over 60 years of experience building compact naval reactors for the U.K.'s Royal Navy, has emerged as a national champion in the race to deploy a domestic SMR fleet. The Rolls-Royce SMR is a powerful 470 MWe pressurized water reactor (PWR), a scaled-down version of the world's most common and well-understood reactor technology. The company's unique advantage lies in its "factory-first" manufacturing philosophy. Rolls-Royce plans to build three dedicated U.K. factories to mass-produce SMR components sized for transport by road, rail, or sea. This assembly-line approach is designed to create a steep learning curve, driving down costs and accelerating schedules for subsequent units.

The U.K. government has thrown its full weight behind the company. In a major validation, the Rolls-Royce SMR was named the "selected technology" in the U.K.'s SMR competition by Great British Nuclear, putting it on a clear path to first deployment in the mid-2030s. The design is in the final stages of the U.K.'s rigorous Generic Design Assessment. Bolstered by this domestic support, Rolls-Royce is now expanding internationally, having formally entered the U.S. regulatory process and exploring opportunities in the Czech Republic and Sweden.