The smart home is no longer a futuristic fantasy—it’s quietly becoming the default. More than half of U.S. households already use at least one connected device. In many new builds, smart locks, learning thermostats, and video doorbells come standard. The result feels like cruise control for daily life—doors unlock when your phone gets close, vacuums clean while you’re out, and leak valves shut before a drip becomes a flood. But what looks like convenience on the surface is powered by a deep stack of technology. Radios, chips, cloud services, and AI software all work together to turn a house into a responsive system. That stack is where the investment opportunity lies. In this report, we explore the top smart home stocks to watch in 2025—curated for pure-play exposure to three core verticals: Control & Security, Specialized Devices, and Enablers & Components.

Why Smart Homes, Why Now?

- First, penetration has tipped from gadget curiosity to mass-market reality. Roughly 77 million U.S. households will use at least one smart home device this year, on track to top 100 million by 2028—about two-thirds of all homes. That demand is powering a global market worth $162 billion today that analysts see racing past $1.4 trillion by 2034, a compound growth rate north of 27 percent. Scale drives prices down; today a Wi-Fi light bulb costs less than a movie ticket, and starter security kits land under $200.

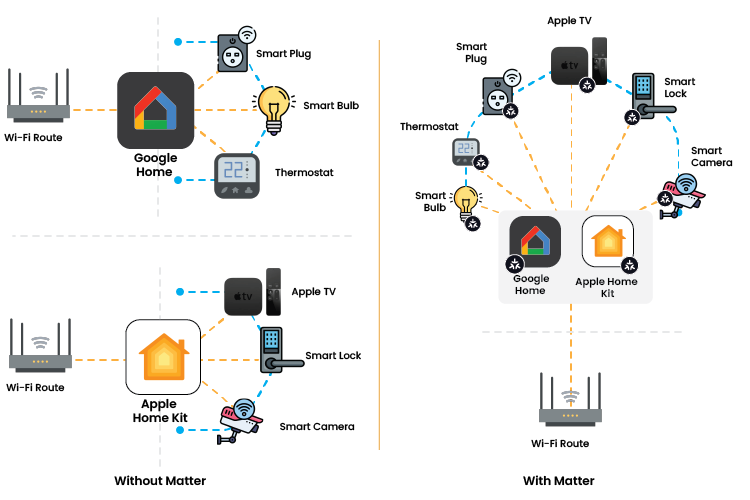

- Second, the technology stack finally speaks the same language. Matter, launched in 2022 and updated twice in 2024, gives everything from fridges to robot vacuums a common protocol. More than 40 device categories are already certified, so a Samsung door lock can now pair with an Apple HomePod without arcane work-arounds. Interoperability removes the “which brand works with which app” fear and unlocks bigger baskets at checkout.

- Third, AI turns raw sensor data into real utility. Cameras no longer just record; they decide whether the blob on your porch is a package thief or the neighbor’s cat. Thermostats predictively pre-heat when traffic data says you’re coming home early. These cloud-based smarts ride on the same breakthroughs driving ChatGPT, making each installed base more valuable over time.

- Finally, macro tailwinds are lining up. Energy prices and carbon rules push utilities to pay homeowners for demand-response, turning every smart thermostat into a revenue stream. Remote work means more time spent at home—and more appetite for convenience, safety and lower bills. Insurance carriers now knock up to 15 percent off premiums for connected leak detectors and security systems, nudging fence-sitters to buy. Meanwhile, chips custom-built for ultra-low power let sensors run for years on a coin cell, cutting maintenance to near zero.

Put it together and smart homes feel less like sci-fi and more like the next phase of consumer electronics—one with recurring revenue baked into every socket. For investors, the story isn’t about a single killer device; it’s the multi-decade shift toward fully networked living spaces and the smart home stocks riding that wave.

Smart Home Control & Security

Think of this layer as the house’s nerve center and immune system rolled into one. Controller hubs, mobile apps, 24/7 monitoring—but the real magic is orchestration: one platform unifies dozens of brands, turning a scattered gadget drawer into a single, self-defending organism. As adoption climbs, these smart home stocks become SaaS businesses wrapped in hardware, taking a small monthly toll every time a front door clicks shut.

Alarm.com (NASDAQ: ALRM)

HQ: USA; SaaS platform for security and home automation.

Alarm.com is the software brain behind thousands of independent security dealers. Its cloud platform ties cameras, locks, thermostats and even EV chargers into one app, then sells that connectivity as a subscription. In 2024, the company posted $631 million of high-margin SaaS and license revenue on $940 million of total sales—its fifteenth straight annual record. Subscription dollars already cover the cost base; hardware sales are simply customer-acquisition fuel.

The moat is two-layered. First, Alarm.com owns the dealer relationship—about 11,000 integrators whose recurring monthly revenue is sticky and hard to dislodge. Second, the feature treadmill never stops: AI video analytics, the new “AI Deterrence” audible-warning service, and a majority stake in CHeKT for remote-video monitoring all landed in the past year.

ALRM benefits from many growth levers. EnergyHub already orchestrates 44 GWh of demand-response events for utilities, while Shooter Detection Systems and OpenEye push the firm up-market into enterprise security where account values are 5–10× higher than residential. With $1.2 billion in cash and no net debt, management can keep buying niche tech without dilution.

Its business model is elegantly simple: spend once to sign up a household, collect monitoring fees for a decade, then upsell analytics and energy modules. Churn sits in the low single digits, leaving a cash-flow machine that compounds almost automatically. If you want exposure to the “rails” of smart home security rather than another gadget maker, Alarm.com is the purest play among smart home stocks.

Resideo Technologies (NYSE: REZI)

HQ: USA; Honeywell spin-off with pro-installed smart home gear.

Resideo is the quiet giant among smart home stocks. Honeywell-branded thermostats, sensors and safety devices are already baked into more than 150 million buildings worldwide, creating an enormous replacement and upgrade annuity. That installed base produced $6.8 billion of 2024 revenue, up 8% despite a sluggish housing cycle.

Now management is stacking software on top of that hardware. In June 2024, Resideo’s ADI distribution arm bought Snap One, instantly adding Control4 automation software, proprietary networking gear and a 17,000-installer community that thrives on recurring service contracts. Snap contributed $553 million of revenue in its first six months and should lift ADI’s margin profile for years.

Product teams are also getting smarter. New thermostat firmware can let utilities shed load during grid stress, smoke/CO sensors self-diagnose, and water-leak valves shut automatically—features that command service fees and meet emerging energy-efficiency rules. Resideo funnels all of this through more than 100,000 professional contractors, a channel DIY rivals struggle to reach.

Net-debt-to-EBITDA sits below 2×, so cash flow can keep funding bolt-on deals or buybacks. Execution risk remains—ADI must integrate Snap without losing focus, and profit still leans on cyclical HVAC volumes—but with a blue-chip brand, swelling software mix, and unmatched dealer network, Resideo looks like a value-priced toll booth on every thermostat a professional installs. If management can nudge service revenue toward even 20% of sales, margins and valuation have room to follow.

ADT Inc. (NYSE: ADT)

HQ: USA; Legacy security brand pivoting to smart monitoring.

ADT is in the middle of a strategic detox. After dabbling in solar and commercial markets, the 150-year-old brand exited residential solar in 2024 and ploughed the savings into debt reduction, a 57% dividend hike, and a new $350 million buy-back. Stripped to its core Consumer & Small Business segment, ADT generated about $4.9 billion of revenue in 2024, up 5% year on year.

The moat is distribution plus data. An exclusive partnership lets ADT installers bundle Google Nest gear while the new ADT+ app unifies monitoring, video and lock control. Google’s face-recognition AI powers “Trusted Neighbor,” quietly unlocking the door for pre-approved visitors and pinging the homeowner when a stranger appears. ADT pays no R&D for that capability yet keeps the lifetime monitoring revenue—an enviable spread.

With solar gone, every dollar of capital now feeds the subscriber engine. Lower hardware subsidies, better self-install kits and tighter churn—attrition hit a record-low 12.6% in early 2025—shrink payback periods to roughly two years. Free cash flow, once weighed down by panel installs, is set to re-accelerate. Debt sits at 3.2× EBITDA and falling, and the company is finally turning the corner from “levered utility” to “sticky SaaS.”

Execution risk is real—service missteps will hit churn—but if management can trade a few points of attrition for growth, the stock’s single-digit multiple leaves plenty of upside. For investors hunting reliable cash flow with an embedded AI catalyst, the new-look ADT deserves a fresh look.

Specialized Smart Home Devices

These smart home stocks are often the headline-grabbers—the robot vacuums, hi-fi speakers, and AI-powered doorbells that solve one clear problem. Each gadget may look like a niche, but together they drive mass adoption by giving people a memorable first taste of “smart.” Over time, specialized devices form a constellation of connected endpoints that feed data, refine AI models, and lock households deeper into their ecosystems.

Arlo Technologies (NYSE: ARLO)

HQ: USA; AI-powered smart camera brand with SaaS upside.

Arlo quietly pivoted from camera-maker to subscription machine. In 2024, services brought in $243 million—53% of revenue—with 81% gross margin and 4.6 million paying accounts. Hardware is now just the on-ramp: sell a doorbell once, harvest monitoring fees for ten years. That flywheel is accelerating. Annual recurring revenue grew 23% to $257 million by December, then blew past $300 million six months later, less than six years after the first paid plan launched.

The moat is data-driven. “Arlo Intelligence” sifts video, audio and Wi-Fi signals to decide whether a shape on the porch is a raccoon or a delivery driver. Origin AI’s wireless-sensing tech and RapidSOS’s 911 pipes add layers competitors lack. Samsung has baked those features into SmartThings, widening reach at almost zero marketing cost. With service margins north of 75% and free-cash-flow margin near 10%, every incremental subscriber drops straight to the bottom line. Management is already using that cash to buy back stock and still finished 2024 with $152 million in the bank and no net debt.

Risks? Google and Amazon loom, and Arlo must keep its AI lead fresh. Yet churn is low-single-digits, and switching means reinstalling every sensor in the house. If ARR keeps compounding above 20%, the market will eventually price Arlo like a SaaS firm rather than a gadget vendor. For investors hunting a pure-play bet on the software rails of home security, Arlo is the one to watch.

Sonos, Inc. (NASDAQ: SONO)

HQ: USA; Premium connected audio with expanding ecosystem.

Sonos sells sound the way Apple sells phones: hardware plus software equals a sticky ecosystem. Fiscal 2024 revenue was $1.52 billion on a stout 45% gross margin, despite an 8% top-line dip tied to a messy app relaunch. The install base now tops 50 million products in 16 million homes, and existing customers created 44% of new registrations last year—proof of an expanding flywheel.

Growth levers are lining up. Ace headphones opened a $5 billion premium over-ear category and just received a “TrueCinema” software upgrade that turns any hotel TV into a spatial-audio theater. The revamped mobile app, rebuilt on a modular code base, should let Sonos bolt on services—think lossless streaming tiers, spatial mixes and maybe even AI-generated tuning—far faster than the old monolith. Direct-to-consumer already accounts for 23% of sales, giving Sonos room to grow margin without middlemen.

Governance risk just reset: long-time CEO Patrick Spence exited after the app fiasco; product chief Tom Conrad is interim boss with a mandate to “ship software that delights,” not chase vanity categories. Balance-sheet firepower helps—Sonos carries no net debt and usually exits each cycle with north of $400 million in cash. The threats are real (Apple’s Vision Pro, relentless imitators), but the recipe hasn’t changed: release a hit box every spring, layer on features every quarter, and let customers add speakers room by room. If the app turnaround sticks, Sonos can get back to its historical mid-single-digit revenue growth while keeping margins elite.

iRobot Corp (NASDAQ: IRBT)

HQ: USA; Roomba maker in deep turnaround mode.

iRobot is deep in turnaround territory, but the brand still matters. After Amazon abandoned its $1.4 billion takeover in January 2024 and paid a $94 million breakup fee, revenue cratered 24% to $682 million for the year. By March 2025 management warned of “substantial doubt” about staying solvent: cash had slid to $134 million while debt sat at $201 million. The stock now trades at a fraction of sales because bankruptcy is on the table.

Yet the tech engine still hums. In March, iRobot rolled out eight new Roomba models with lidar mapping, spinning mop pads and Matter smart home support—its biggest refresh ever. All run iRobot OS 7, whose Dirt Detective AI decides which rooms need extra passes and automatically switches from mop to vacuum. That shift catches up to Chinese rivals on hardware while leaning into iRobot’s long-held software edge. Over 50 million robots sold since launch give the company a treasure trove of cleaning data competitors envy.

New CEO Gary Cohen is slashing 31% of staff and targeting $150 million in annual savings, aiming to push gross margin back above 30% and free up R&D dollars for AI features. The thesis is simple: refinance the balance sheet, prove demand for the lidar lineup, and position iRobot as an attractive bolt-on for an appliance or tech giant once regulators cool. Among smart home stocks, it’s a high-risk, high-reward bet—either a zero or a multi-bagger if the Roomba brand cleans up its own mess.

Smart Home Enablers & Components

Behind every blinking thermostat and talking speaker sits an invisible cast of chipmakers, protocol gurus, and networking vendors. These smart home stocks are the “picks and shovels”, supplying silicon, firmware, and antennas so brands can launch products faster and cheaper. When a new wireless standard wins or AI workloads shift to the edge, enablers reap the upside across hundreds of device categories at once.

Silicon Laboratories (NASDAQ: SLAB)

HQ: USA; Wireless chipmaker for Matter and IoT devices.

Silicon Labs is the quiet king-maker of the smart home stack. Its chips hide inside everything from Zigbee light bulbs to Matter-ready door locks, making the company a “picks-and-shovels” play on every connected device sold. 2024 revenue was $584 million, all generated by low-power wireless SoCs and the software that drives them.

What keeps designers coming back is one-chip flexibility. February’s MG26 platform runs Bluetooth LE, Thread, Zigbee—and Wi-Fi—at the same time, with built-in AI/ML blocks for tasks like face detection or energy-harvesting control. That means fewer parts on the circuit board and faster certification—catnip for appliance OEMs racing to add Matter without blowing their BOM.

Scale reinforces the moat. Silicon Labs has now shipped more than 10 million Wirepas mesh chipsets for smart meters and streetlights, proof it can win industrial volumes as easily as doorbell sockets. Its Simplicity Studio tool chain, huge library of protocol stacks and bulletproof security labs create switching costs that a spec sheet can’t capture.

The upside? Matter adoption is still in early innings, Wi-Fi 7 will push new upgrade cycles, and every additional protocol the company supports widens its addressable market. Because Silicon Labs is fabless and asset-light, incremental dollars drop straight to cash that can fund yet another protocol, buy niche IP, or simply flow back to shareholders. If you want broad exposure to whatever wireless standard wins the living-room war, owning the toll-collector instead of a brand name gadget could be the smarter bet.

Ubiquiti Inc. (NYSE: UI)

HQ: USA; Pro-grade networking gear with consumer simplicity.

Ubiquiti sells “pro-grade, consumer-simple” networking gear—and does it with almost no marketing budget. Fiscal 2024 revenue hit $1.9 billion, powered by word-of-mouth demand for its UniFi access points, Protect cameras and switching gear. Founder-CEO Robert Pera keeps overhead lean so gross margins can stay fat even while prices undercut Cisco and Arista.

Tech is the hook. This year’s UniFi 7 line packs twelve spatial streams and beam-forming antennas that serve gigabit Wi-Fi across cafés, warehouses or McMansions. Because the same UniFi Controller software also manages security cameras, doorbells, VoIP phones and routing, every new product sinks teeth deeper into the customer. No subscription fees, local video storage and an Apple-like interface turn clients into evangelists.

The community is the moat. An army of installers and Reddit power users troubleshoot problems for free, slash support costs and act as a 24/7 focus group. That feedback loop lets Ubiquiti iterate hardware annually—often shipping beta firmware in days, not quarters. Analysts call the model risky; Pera calls it a “flywheel you can’t buy with ad spend.”

Looking forward, Wi-Fi 7, AI-assisted camera analytics and an expanding ISP-grade “UISP” platform open fresh markets without changing the cap-light DNA. Supply-chain snarls and the founder’s tight grip will always add volatility, but if you believe the networking world wants Apple-level polish at half the price, Ubiquiti is already there—and compounding quietly.

Nordic Semiconductor (OTCMKTS: NDCVF)

HQ: Norway; Bluetooth and cellular IoT chip specialist.

Nordic is the Bluetooth LE specialist that ships in Fitbits, smart locks, and most of the tiny sensors you never see. 2024 revenue came in at $511 million—down only 6% despite the IoT glut—thanks to design-win momentum and best-in-class power draw.

Now the fourth-generation nRF54 family is resetting the bar. The new nRF54L series cuts power further, doubles processing headroom and bakes in cryptographic accelerators for Matter and Thread. Its big brother, the nRF54H20, just nabbed a global “Wireless Product of the Year” award, signaling strong early traction.

But Nordic isn’t staying Bluetooth-only. The nRF9151 System-in-Package wraps LTE-M, NB-IoT, GNSS and future satellite support into a stamp-size module ready for asset trackers and smart meters. One PCB swap moves customers from room-scale to continent-scale coverage—again with Nordic’s trademark frugal battery draw.

The playbook is simple: ship reference designs, flood GitHub with code, and let a million hardware startups do the selling. Once a device is qualified, ripping out the radio means new certifications and firmware rewrites—sticky by design. As IoT demand rebounds and Matter pulls wireless into every appliance, Nordic’s “lowest-power-wins” mantra should translate into share gains and margin expansion. Among smart home stocks, Nordic represents a pure, leveraged bet on the next billion battery-powered widgets.